Terms on this page

Loveland FY 2026 General Fund — the actual numbers

The trade documented in this chapter is small in relative terms next to the city’s overall General Fund, which is why the framing “we cannot afford a shelter” ran in parallel to a permanent enforcement-staffing commitment that the same fund absorbed without comment.

- FY 2026 General Fund revenues

- $128.0 million

- FY 2026 GF operating expenditures

- $127.6 million

- FY 2026 GF capital + transfers + debt

- $6.8 million ($4.5M capital projects + $2.3M equipment replacement and debt)

- FY 2026 total GF expenditures

- $134.4 million

- Ord 6807 General-Fund slice

- $95,989 · 0.075% of the FY 2026 GF total

- Four new PD positions, recurring

- $1,187,274 / yr · 0.93% of GF, every year · OpenGov line-item total

The Citizens’ Finance Advisory Commission — the city’s own volunteer body chartered under LMC 2.60.060 to review the budget — adopted a resolution accompanying the FY 2026 first reading that included this finding in its own words:

Citizens’ Financial Advisory Committee recognizes the unsustainability of the current budget with regard to the capital maintenance needs of the City. Any unforeseen non-recurring excesses should be used exclusively for critical capital maintenance needs. — CFAC Resolution, 18 September 20258

The resolution was adopted thirty-three days before the Council passed the same FY 2026 budget on second reading (8-0, 21 October 2025) carrying the four new sworn LPD positions, and one hundred and ten days before the Council voted 6-3 to spend $2.85M on the shelter purchase. The General-Fund slice of that purchase — $96K — would have been one third of one percent of the “non-recurring excesses” CFAC named as the only legitimate target for new spending.

What a Capital Expansion Fee is

Loveland established Capital Expansion Fees (CEFs) in 1984, becoming one of the earliest Colorado adopters. CEFs are impact fees the city collects from developers on new construction, segregated by category, and legally restricted to capital projects with a rational nexus to the category they were collected under. The framework derives from Krupp v. Breckenridge and subsequent Colorado case law.

Active CEF funds as of the FY 2026 budget book include:

- General Government CEF (Fund 268)

- Police CEF

- Library CEF

- Cultural Services CEF

- Parks CEF

- Recreation CEF

- Trails CEF

- Open Lands CEF

- Streets / Transportation CEF (largest single category)

Per a 2018 staff memo, total CEF balances across all categories were ≈ $40M at end of Q1 2018. The General Government slice is meaningful but not the largest.

How Ord 6807 was sourced

- Total appropriation

- $2,850,000

- From CEF Fund 268

- $2,754,011 · 96.6 %

- From General Fund

- $95,989 · 3.4 %

The political effect of that split is that the headline number reads as “$2.85 million of spending” while the taxpayer-felt General-Fund cost is under $100,000. The $2.75M from Fund 268 is restricted and could not have been redirected to police salaries, library hours, or utility-bill relief — but it could have funded other General Government capital projects (municipal-building renovation, fleet expansion, IT facility upgrades) that are on hold during the austerity.

The shelter was not funded with “free money.” It was funded by displacing other planned general-government capital spending.

The nexus problem

A homeless shelter does not obviously sit within the General Government CEF nexus. The fee was collected on the theory that new development creates demand for general government capacity — city hall space, fleet, administrative buildings. The argument that new development creates demand for homeless shelter capacity is harder to defend, because the population needing the shelter is typically not the population generating the developer fees.

City staff almost certainly walked through this and concluded the theory was defensible on the basis that the building, while used as a shelter, would be a city-owned operational facility serving a citywide function. The conditional structure of the deal (purchase only if a nonprofit operator commits) may have been partly designed to keep the city’s role on the “facility owner” side of the line rather than the “shelter operator” side, preserving the nexus argument.

Whether any opinion letter from the City Attorney’s office was prepared evaluating nexus before the 6 January vote is a CORA target.

The parallel General-Fund commitment

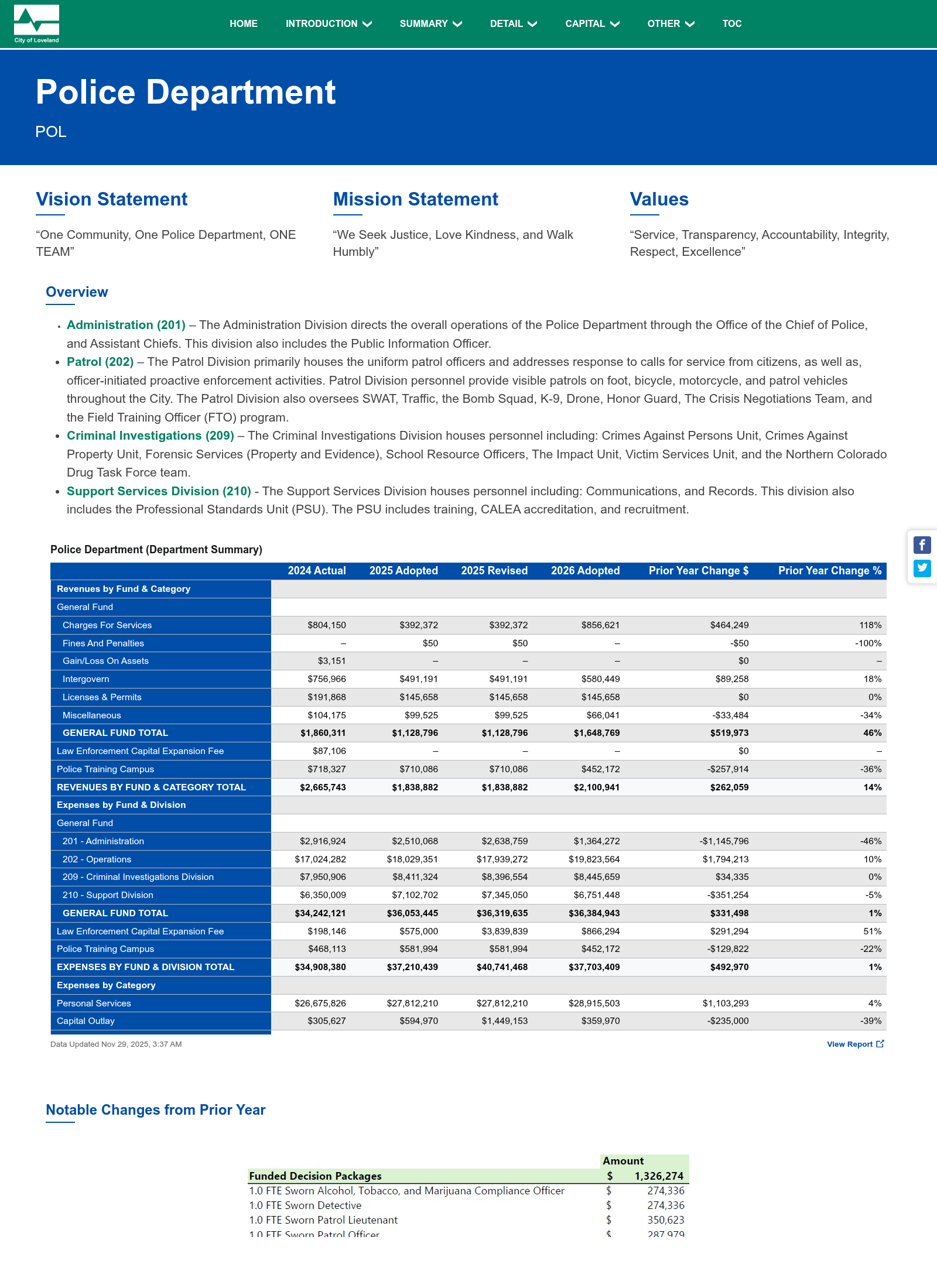

The 2026 budget — adopted 21 October 2025 — added four new Police Department positions:

| Position (OpenGov line item) | First-year cost | Source of funds |

|---|---|---|

| 1.0 FTE Sworn Patrol Lieutenant | $350,623 | General Fund |

| 1.0 FTE Sworn Patrol Officer | $287,979 | General Fund |

| 1.0 FTE Sworn Detective | $274,336 | General Fund |

| 1.0 FTE Sworn Alcohol, Tobacco, and Marijuana Compliance Officer | $274,336 | General Fund |

| Four-FTE subtotal, annual, ongoing | $1,187,274 / yr | |

Figures are the City’s own line-item Funded Decision Package totals as published in the FY 2026 budget book on OpenGov (PD detail page), not loaded-cost estimates — they already include salary, benefits, equipment, training, vehicle, and supervision. Source: OpenGov · Police Department — Funded Decision Packages (2026 Adopted) · local archive HTML shell · rendered table PNG.

{kind=link}

LPD on the record: no staffing change tied to Ord 6806

The four new sworn FTEs were locked into the FY 2026 budget on 21 October 2025 — eleven weeks before Ord 6806 (the anti-encampment amendment) reached first reading, and fifteen weeks before its second reading. On 3 February 2026, during the Ord 6806 second-reading debate (Cablecast #669), a Loveland Police Department official testified on the record — in response to direct council questioning about enforcement workload — that the amendment would not change staffing.

“We respond to every call for service that comes into our dispatch center. We’re not anticipating a staffing change or anything like that at this point. No, we’re not doing any staffing changes based on this.” — LPD official, in response to council questioning, 3 February 2026

This is the on-record refutation of the “enforcement requires more officers’ budget” rhetorical structure that the four-FTE addition was sometimes positioned to satisfy. Ord 6806 operates on existing LPD staffing levels with no expansion request tied to it. The four FTEs added in October 2025 were a separate, prior commitment — and the OpenGov line item for the fourth position confirms it was a marijuana / alcohol / tobacco compliance officer tied to the 2027 retail-marijuana rollout under Measures 2F and 2H, not an encampment-enforcement hire. The temporal order and the line-item description both rule out the post-hoc “we needed these officers for Ord 6806” framing. Full clip transcript and the surrounding meeting context are in /transcripts/#police-staffing.

The Compliance Officer position is the most plausibly tied to enforcement of the updated encampment ordinance (Ord 6806), though no city record explicitly links them. The position description itself is a CORA target.

The trade, expressed as cashflow

- Shelter purchase (had it closed)

- $2.85M one-time · 96.6 % from restricted CEFs · ≈$96K from General Fund · operations contracted out to nonprofit · sunset effectively at 2027

- Four new sworn positions (already approved)

- $1,187,274 / year · 100 % General Fund · permanent recurring · no sunset

- LRC sale proceeds (planned)

- ~$410K one-time · returns to General Fund · offsets ~4× the shelter package’s General-Fund slice

Over a ten-year horizon, the enforcement-and-staffing pivot is approximately $11.87 million in committed General-Fund spending (before any salary-growth, COLA, or pension-contribution escalation; the four FTE base totals already include benefits and loaded costs as scored in the OpenGov budget book). The shelter purchase, had it closed, would have been a one-time $96,000 charge to the General Fund, partially or fully offset by the LRC sale proceeds. In strict General-Fund terms the enforcement-and-staffing pivot is materially more expensive than the shelter would have been — and continues forever.

Where the $2.85M is now

The funds didn’t leave the city’s accounts — the purchase never closed. They’re still in three buckets:

| Bucket | Amount | Status |

|---|---|---|

| General Fund slice | ≈ $95,989 | absorbed into reserves; untrackable |

| General Government CEF (Fund 268) | ≈ $2,754,011 | sitting in restricted reserves; available for future general-government capital projects |

| LRC building (137 S Lincoln) | ≈ $410K + | still owned by city; planned to be sold |

Tracking Fund 268 over the next 12–18 months will reveal whether the CEF reserves get used for police facility expansion, get held as capital ballast against the 2027 marijuana revenue forecast, or simply sit until another General Government capital need arises.

The 2027 proposed budget book (typically released August–September 2026) is the next public document that will show the answer.

The trade in one picture

The other public-money channel — Centerra URA (preview)

The General-Fund / CEF trade above concerns ≈$95K in unrestricted general fund spending and the future of ≈$2.75M in restricted impact-fee reserves. The City’s other large public-money channel — the Centerra Urban Renewal Plan, which has moved more than one billion dollars in taxpayer-supported revenues to a developer-controlled metropolitan district since 2004 — was the subject of a forensic audit by Ernst & Young delivered on 14 October 20256 .

The Phase I deliverable findings:

- Scope reviewed

- 5,587 files · 90,000 GL transactions · 73 cash disbursements + 9 public bid awards sampled (back to 2009) · cumulative cash flows ~$1.26B; $88.4M project spend + $39.6M non-project spend; $18.4M Phase 2 scope; $34.5M PIC→CPW untested in Phase 1

- Public-bid testing universe

- $51.1 million in publicly-bid awards 2015–2023 (testing universe)

- Project spend potentially-should-have-been-bid

- $6.2 million (precise: $6,221,959; 30 transactions; 7.0% of project spend) identified as project spend not subject to public bid but potentially-should-have-been-bid depending on the interpretation of “Construction” in the MFA

- Related-party payments to McWhinney

- $4.9 million to McWhinney Real Estate Services since 2009 for management, landscaping, and marketing — without arms-length documentation

- Water-rights transfer pattern

- McWhinney-related entities transferring water rights to the metro district without any written analysis of fair-market pricing

- Board recusal pattern

- Metro district board members with declared employment or financial interests in McWhinney firms did NOT recuse themselves from related-party votes

- Internal-control findings

- Invoices coded to wrong GL accounts · missing approvals · payments in wrong financial periods · no monthly financial close by district manager

These findings — published a month before the FY 2026 budget vote

and four months before the City approved the Costco Business Assistance

Agreement committing identifiable contractual city financial components on

the order of $25–$100M+ over 25 years (composition

buildup in Chapter 06; fact card

facts/f3e) to a McWhinney-affiliated entity — were what

Mayor McFall instructed the public-comment record to disregard on

17 February 2026. See Centerra for the full audit

detail and Recall for the resulting First Amendment lawsuit.

Centerra MD-1 2026 adopted budget — the $22.9 million annual call

The Centerra Metropolitan District No. 1 board adopted its 2026 budget at the same 16 October 2025 meeting whose record-of-proceedings shows nine Pinnacle Consulting staff, two McWhinney-company observers, and the district president (who is also a Realberry employee) in the room. The numbers in that budget are the second piece of the comparative scale the trade above operates inside.

- 2026 Debt Service Fund total revenues

- $22,924,542

- 2026 Debt Service Fund total expenditures

- $22,910,163

- Series 2017 bond principal · 2026

- $12,280,000 · up from $9,995,000 in 2025 — escalating amortization

- Series 2017 bond interest · 2026

- $6,674,250

- Series 2018 bond interest

- $583,013 / yr (constant)

- Series 2020A bond interest

- $1,621,750 / yr (constant)

- Series 2022 bond interest

- $1,664,650 / yr (constant)

- CMD-1 mill levy · 2026

- 0.000 mills · District No. 1 itself levies no property tax; the residential sub-districts (Districts 2-5: Railway Flats 43.5, Kinston 43.0, Avenida 46.8, District 5 15.6) carry the load

- 2026 Capital Projects Fund expenditures

- $10,612,935 · deficit-spent from prior bond reserves

- Revenue source not on the rolls

- Public Improvement Fee (PIF) — 1.25¢ on retail sales inside the Commercial District, imposed and collected by the Centerra Public Improvement Collection Corporation (PIC) and distributed downstream9

The comparative arithmetic is the point of putting both budgets on the same page. Loveland’s entire FY 2026 General Fund capital-projects budget is $4.5 million. Centerra Metropolitan District No. 1 spent more than twice that figure — $10.6 million — out of bond reserves in 2026 alone, while paying out $22.9 million in debt service the same year, secured by mill levies on residents of the underlying districts. That latter figure — one Centerra metro district’s annual call on Centerra residents’ tax bills — runs five times the city’s own General-Fund capital-projects budget.

These two budgets do not move dollars between themselves directly. They are

parallel public-money structures sharing a developer, a counsel, an

administrator (Pinnacle Consulting), and, on 17 February 2026, a single 8-1

vote in which the city committed identifiable contractual financial

components on the order of $25M (bond/PIF cap) + $11M (Kendall

cash) + $6.5M (developer reimbursement) ≈ $42.5M to the same

counterparty over the next twenty-five years, with AIR-102809 projecting

“over $100MM” of retained sales-tax revenue back to the city

over the same horizon (composition buildup in

Chapter 06; fact card

facts/f3e).

The dark-money superstructure

Three independent expenditure committees registered with the Colorado Secretary of State share a common consulting vendor and overlap in donor geography and target races. Together they form what TRACER bulk data records as a Northern Colorado Republican-aligned political infrastructure:

- Strong Colorado IEC (CO 20245047480)

- $12,050 raised · Centerra Properties West $9K + Sethre $2K + Fogle/Dinsmore $500 each · funded the Krenning recall canvassing

- NoCo Reboot (CO 20195037700, Windsor)

- $22,652 raised · The Revere Initiative 501(c)(4) $15,752 + CO State FOP SDC $6,900 · spent on Buzz360 (texts), Brandzooka (digital), Polifi (consulting)

- Justice for Jason (CO 20245046974)

- $42,000 raised solo · Patricia Telleen (Fort Collins) · spent $36,825 with Street Media Group LLC (Gary Young, 5747 Nicklaus Dr) + monthly retainer to Polifi

- Common consulting vendor

- Polifi LLC · $312,870 in 2024-2026 TRACER receipts across ~20 R-aligned committees (Kirkmeyer, Carlos for HD 48, Woog HD 19, Brauchler for DA, Lori Garcia Sander for HD 65, Montoya for Sheriff, four county R central committees)7

- Common ad vendor

- Street Media Group LLC · Gary Young, 5747 Nicklaus Dr Fort Collins · received $36,825 from Justice for Jason and ads-business from NoCo Reboot · same operator runs The Revere Initiative 501(c)(4) that funds NoCo Reboot

- Colorado State FOP SDC (CO 19991400287) selected disbursements

- $6,900 → NoCo Reboot · $10,000 → Senate Majority Fund · $5,000 → Committee for a Safer, Stronger Denver · $3,100 → Dawn Downs for DA · plus contributions to R candidates in HD 19, 39, 48, 64, 65

None of this money flows directly to Loveland municipal council races (which are not in TRACER — state-level only). The structural connection to the Loveland Council, where it is documented, is the Strong Colorado IEC recall vehicle whose largest single donor is the same McWhinney-affiliated entity whose Costco BAA the resulting council majority approved.

Primary Sources

- 1 filing City Council Voting Results — December 16, 2025 (Ord 6803 supplemental, PCAB appointments), City of Loveland · CivicWeb, [local archive]

- 2 filing FY 2026 Adopted Budget · General Fund + Police Department, City of Loveland Finance,

- 3 filing City Council Voting Results — February 3, 2026 (Ord 6806 anti-encampment 5-4), City of Loveland · CivicWeb, [local archive]

- 4 press Centerra audit finds bidding, accounting lapses in Loveland, Loveland Reporter-Herald,

- 5 data Strong Colorado IEC · contributions and expenditures, Colorado Secretary of State TRACERaccessed

- 6 audit Ernst & Young Phase I deliverable summary (LURA board, 14 Oct 2025), Loveland Reporter-Herald,

- 7 data Polifi LLC payee aggregate across CO committees, 2024-2026, Colorado Secretary of State TRACER (bulk expenditure data)accessed

- 8 filing Loveland FY 2026 Budget — first reading packet, Attachment 3: CFAC Resolution recommending 2026 budget process and adoption (18 Sept 2025), City of Loveland · Citizens' Finance Advisory Commission,

- 9 filing Centerra Metropolitan District No. 1 — 2026 Adopted Budget (Doc 65282, adopted 16 Oct 2025), Centerra Metropolitan District No. 1,